China's New Rare Earth Metal Dominance is a Monopoly for the Age of EVs

China’s regulation of its BigTech sector has caused waves, with firings at multiple companies including for instance IQiyi and ByteDance, among many in the Ed-tech sector. While this has baffled Western investors, China thinks long-term.

This week China has also done something else a bit surprising. China’s new rare earth merger hands it ‘trump card’ in global fight for resources. China has a rare monopoly on rare earth metals, along with its incursion into Africa. China approved a merger of key rare-earths companies, creating a behemoth that will strengthen its control over the global sector it has dominated for decades.

China Rare Earth Group

The new firm will be called China Rare Earth Group and will be based in resource-rich Jiangxi province in southern China as soon as this month, the people said. The new entity would be created by merging rare-earths assets from some state firms, including China Minmetals Corp. , Aluminum Corp. of China Ltd.

As of 2018, China had 44 million tonnes or 36.7 per cent of the world's rare earth deposits, Brazil has 22 per cent, Vietnam 18 per cent, Russia 10 per cent and India has 5.8 per cent. The rest of the world, including the US and Japan, have 10.9 per cent of rare earths. It’s not by accident that China has gotten more powerful in South America and Africa.

China’s Weird Dominance in Rare Earth Metals

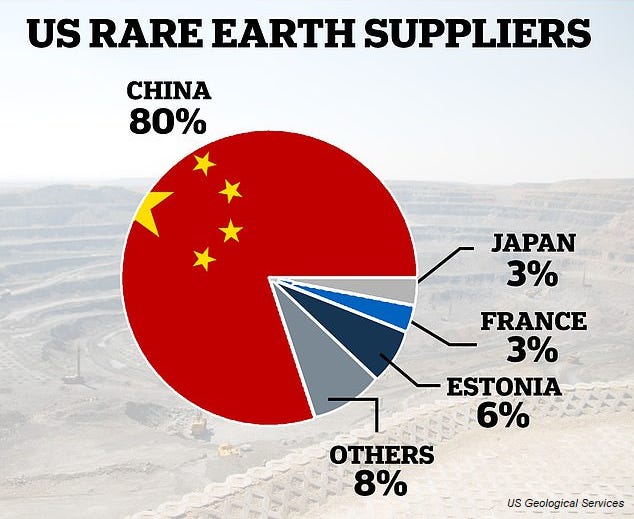

In 2019, China was responsible for 80% of rare earths imports, according to the U.S. Geological Survey, although exports fell last year in part due to Covid-19. While the U.S. has been able to regulate some of Chinese companies like Huawei and recently SenseTime’s IPO, not everything can be regulated.

Rare earths elements are more abundant than their name suggests but extracting, processing and refining the metals poses a range of technical, political and environmental issues. America has basically failed in the last decade to secure its future with rare earth Metals.

Some hardliners have urged Beijing to weaponize its dominance in rare earth production after the Trump administration started a trade war in 2018. China has wolfish and panda camps that differ on how to handle global diplomacy. Increasingly China is taking a hard stance against other countries and companies that don’t fall in line with its own agenda.

The Biden administration and Department of Energy have targeted rare earths among domestic supply chain priorities as they outline ambitious climate and technology policy. Outside of Tesla, America is not so well positioned with Rivian, Lucid, GM and Ford to do much in the EV sectors against China’s own EV startups that have at least a dozens serious contenders.

As the market for EVs expands rapidly, the demand for components like electric motors does so along with it. In 2021, the demand for EV motors is expected to increase by 40% in the car market alone.

Electric motors literally drive EVs, but many designs utilize kilograms of magnetic materials. These magnets rely heavily on rare-earth materials like neodymium and dysprosium, which are expensive, produce lots of waste and have various mining concerns. Will EV manufacturers continue to rely so heavily on rare earths going into the future?

In 2019, China was responsible for 80% of rare earths imports, according to the U.S. Geological Survey, although exports fell last year in part due to Covid-19. It seems China anticipated what EVs would need and prepared many years in advance.

The supply chain for rare earths is extremely constrained geographically. China accounts for the vast majority of worldwide production which has historically led to price volatility. Back in 2011, China restricted exports of rare earths seeing an approximate price rise of 750% and 2000% for neodymium and dysprosium respectively.

China’s Power Play in Rare Earth Metals

With the recent merger, China is able to corner the market in rare earth metals in a dominant way.

The entity will be formed through merging rare-earth units of government-owned companies including China Minmetals Corp., Aluminum Corp. of China and Ganzhou Rare Earth Group Co., according to a stock exchange filing from China Minmetals Rare Earth Co. The new group will accelerate the development of mines in the south, CCTV reported.

China’s move to set up a global force in the strategic rare earth sector could help it pre-empt and respond to future external challenges, including trade tensions with the United States, analysts say.

As far back as the Spring of 2019 China was considering limiting exports of Rare Earth Metals to the U.S.

China can Nationalize its biggest companies in way that mean its own business secor will have significant advantages and leverages becoming monopolistic on the global state in the decades ahead.

Two Super Companies Consolidate China’s Monopoly on Rare Earth Metals

The government is aiming to eventually consolidate all its rare earth miners and processors into the two huge firms, one in the north and one in the south, the people said, asking not to be identified discussing a private matter.

The one in southern China will oversee medium-to-heavy rare earths, and the other in the north will control all light rare earths, the people said. It’s unclear when the merger will be completed.

While China is dominant now, in the decades before the 1980s it was the U.S. that held a majority stake in this metals market. That changed as production growth abroad and mounting environmental pressures at home shifted production overseas and also offered cheaper labor costs. According to one 2018 report from the Department of Defense, China “strategically flooded the global market” with rare earths at cheaper prices to drive out and deter current and future competitors.

It’s not that China doesn’t understand Capitalism or want to participate in it, it’s just that it does things a bit differently. Beijing has been restructuring the industry for years into six large state-controlled groups. By consolidating, it hopes to maintain its dominance in the production of the strategic metals, of which it controls 70%, as the U.S. and Europe look to develop their own production and supply chains and diversify away from China. It’s Government wants to be able to pick the winners.

Which Rare Earth Metals Are Important?

The three most important materials used in magnets include neodymium, dysprosium and terbium. Terbium is one of the toughest to come by because production, extraction and magnet-making are focused on China. Trade wars and retaliatory tariffs can leave many companies sourcing these crucial materials in limbo, even if they make up just a small portion of a product.

Beijing’s decision almost 30 years ago to make rare earths a strategic material and ban foreigners from mining them helped pave the way for China to elbow aside the U.S. as the world’s leading producer. The minerals’ biggest usage is in permanent magnets, which include the NdFeB variety, found in everything from phones to computers to cars.

Now with supply chains dysfunctional for what could be years, China’s plan is coming to fruition in sectors like the future of electric vehicles. Demand for rare earths -- a broad group of 17 elements -- is rising, driven by growing need for permanent magnets.

In 2020, 77% of the electric car market used permanent magnet motors, a ratio that has remained fairly consistent over the past 5 years. Although the U.S. is making strides to advance the rare earths supply chain and develop alternatives to mining rare earths, environmental regulations are often more stringent than inside China.

China Beat the U.S. To Dominate the Market of Rare Earth Metals

We don’t know yet know the full costs of China winning the Rare Earth Metal market dominance in 2022 yet. At the end of September, 2020 U.S. President Donald Trump released an executive order amounting to an all-hands-on-deck call to end China’s monopoly on rare earths, the metals and alloys used in many high-tech devices. But the U.S. were careless in this regard.

China’s dominance of these resources has resulted in the transfer of entire U.S. industries (medical imaging, for example), technologies, and jobs to China while also compromising the U.S. defense industry’s supply chain. China outfoxed the U.S. over the last thirty years. In fact, up until 1980, 99 percent of the world’s heavy REs were a byproduct of U.S. mining operations for titanium, zircon, and phosphate.

As of December, 2021 some analysts say China mines more than 70% of the world's rare earths and is responsible for 90% of the complex process of turning them into magnets, analysts say. A White House report has estimated that China controls 55% of the world's rare-earth mining and 85% of the refining process, according to the WSJ.